Simple Regime Switching for SP500

|

| image from http://brucekrasting.com/ |

Let us consider two possible ways to trade the SP500.

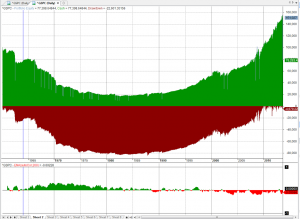

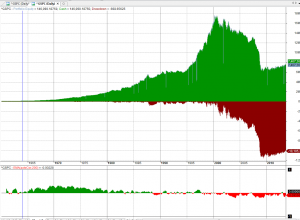

1. If the index falls today, we buy tomorrow at the open. This is a "mean-reversion" strategy. 2. If the index rises today, we buy tomorrow at the open. A "follow-through" strategy.

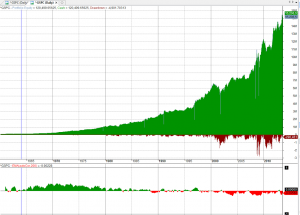

From the graphs below, we can see that neither of these strategies worked well from 1960 to today.

Let's introduce a qualifier that will tell us which strategy to trade at what time.

We will try the most basic one: The correlation between today's return (close to yesterday's close) to the previous day's return. If it is negative we 'll use a contrarian logic. If the correlation is positive we 'll use a momentum logic.

The indicator of choice is the 2-period Relative Strength Index (RSI).

So if correlation between yesterday's and today's return is less than zero we buy on a correction. Otherwise we buy on strength. We trade at the next Open.