Day of month effect on rebalancing a portfolio

In this post we will:

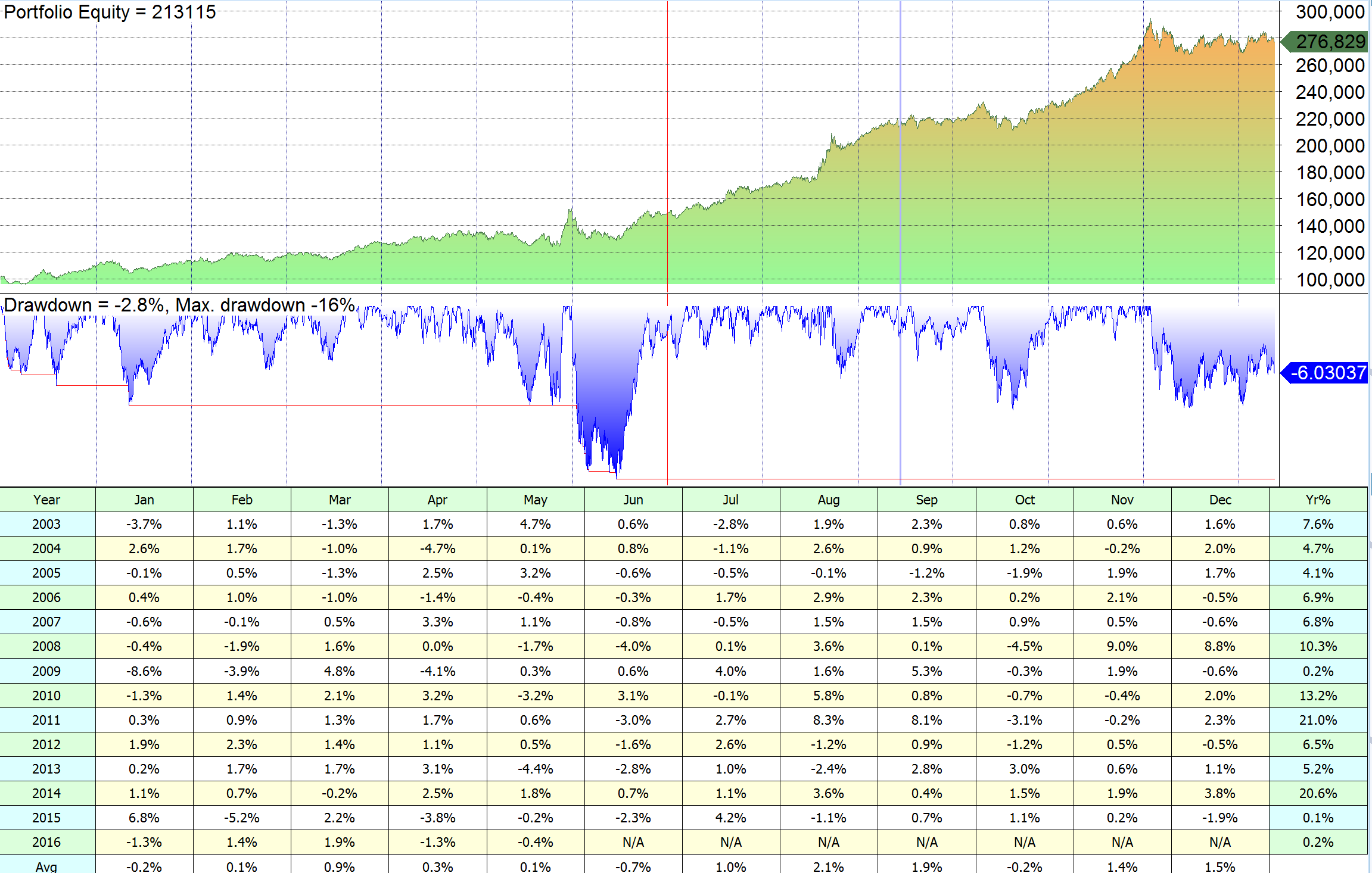

- Take a look at a simple, momentum based, monthly rebalanced Equity/Bond portfolio consisting of two ETFs: SPY and TLT.

- Search for what has been the optimal dates in the month to rebalance such a portfolio.

Each month we allocate to SPY and TLT.

If SPY has outperformed TLT we rebalance to 60% SPY - 40% TLT.

If TLT has outperformed SPY we rebalance to 20% SPY - 80% TLT.

For the first run we will re-balance on the first of the month and close at the last day of the month.

Now will try different combinations of entry and exit days.