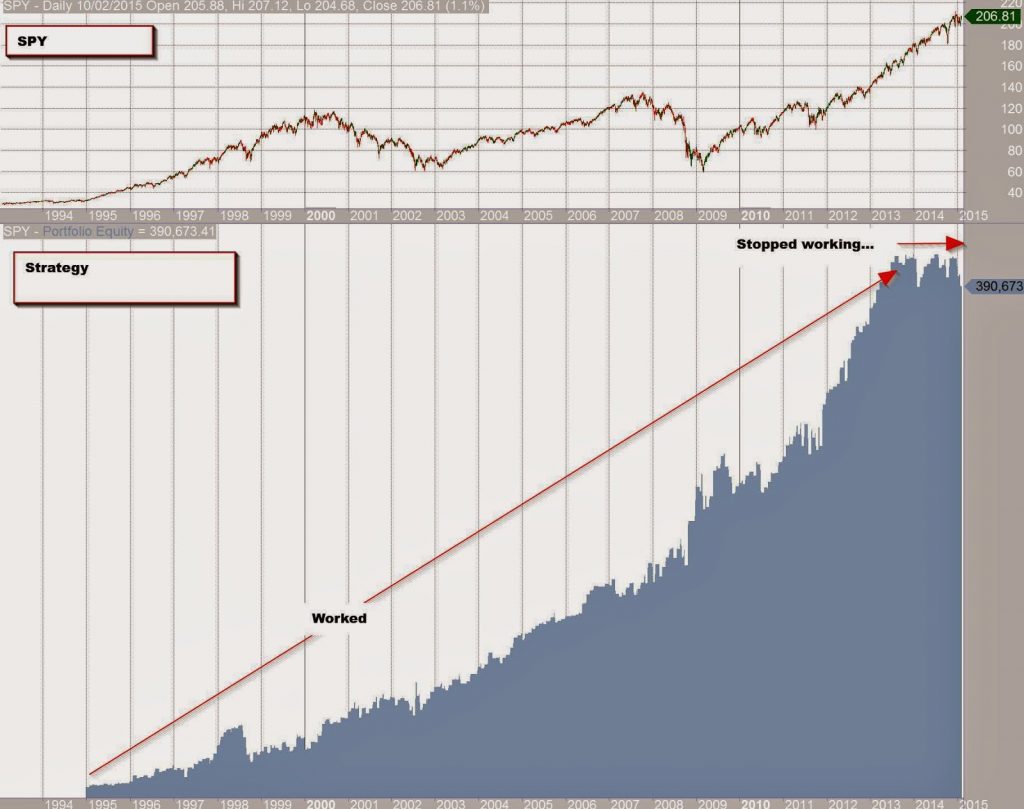

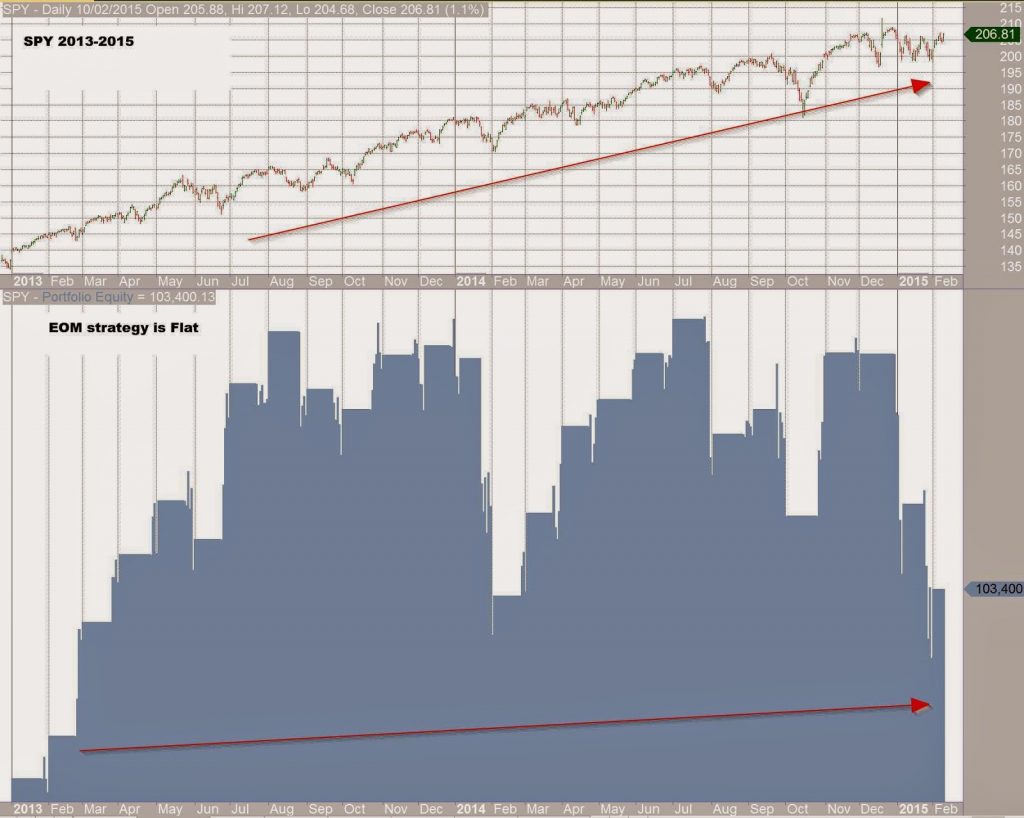

The end of the end of month strategy

Has the end of month strategy stopped working?

This has been well documented in academic papers as well as blogs. The main reason quoted for this persistent bias has been end-of-month window dressing.

As one of my favorite author/blogger/trader, Mr. Grøtte, has also recently blogged the EOM bias is no more.

Why is this important to know?

A lot of investors re-balance monthly. The day of the re-balance used to be somewhat important as there was an EOM bias. So it was better to 'buy' at the end of the month rather than at the beginning of the month. As of late (2013) this is less true.

What this means in practice is that the specific timing for re-balancing monthly strategies may be less important than it used to be.

//Amibroker code:Buy=Day()>=23 AND CMA(C,100);Sell= (Day()<11 AND C>Ref(C,-1));SetTradeDelays(0,0,0,0);slip=0.00;BuyPrice=c+slip;SellPrice=c-slip;posqty=Param("nUMBER OF pOSITIONS",1,1,30,1);SetOption("MaxOpenPositions",posqty);PositionSize=- 98/posqty;bars = 10; // exit after 10 barsApplyStop( stopTypeNBar, stopModeBars, bars, True );

Related post

The Bull Bear Bitcoin Strategy at TokenSets.com

+ I will be managing the Bull Bear Bitcoin Set (symbol: BBB)…

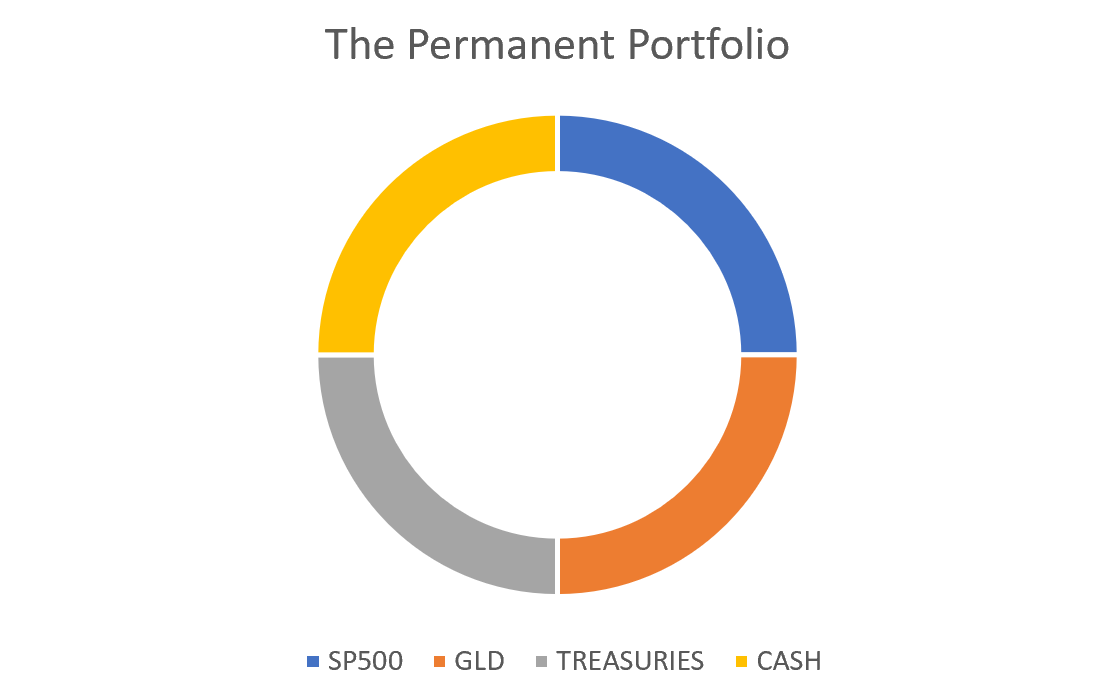

Enhancing Harry Browne’s Permanent Portfolio strategy

First published at Logical-Invest.com Harry Browne’s intention was to find a solution…

Intro to rules based Investing - Why follow an investment strategy?

1. Basics What is rules based Investing? In rules-based-investing we define a…

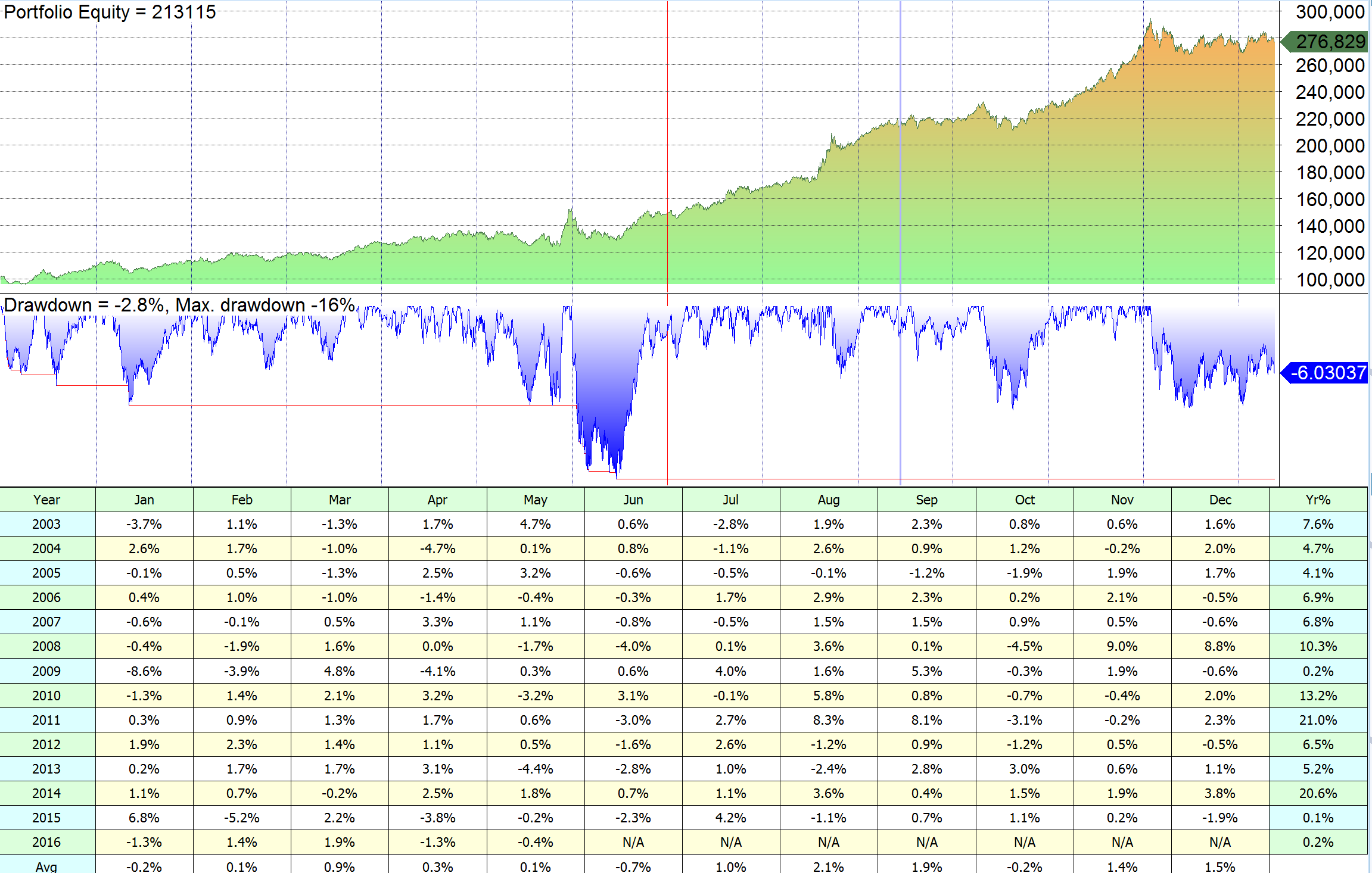

Day of month effect on rebalancing a portfolio

In this post we will:

- Take a look at a simple, momentum based, monthly rebalanced Equity/Bond portfolio consisting of two ETFs: SPY and TLT.

- Search for what has been the optimal dates in the month to rebalance such a portfolio.

Each month we allocate to SPY and TLT.

If SPY has outperformed TLT we rebalance to 60% SPY - 40% TLT.

If TLT has outperformed SPY we rebalance to 20% SPY - 80% TLT.

For the first run we will re-balance on the first of the month and close at the last day of the month.

Now will try different combinations of entry and exit days.