7 Winning Trading Systems Reviewed - Pt. 3: RSI 25 75

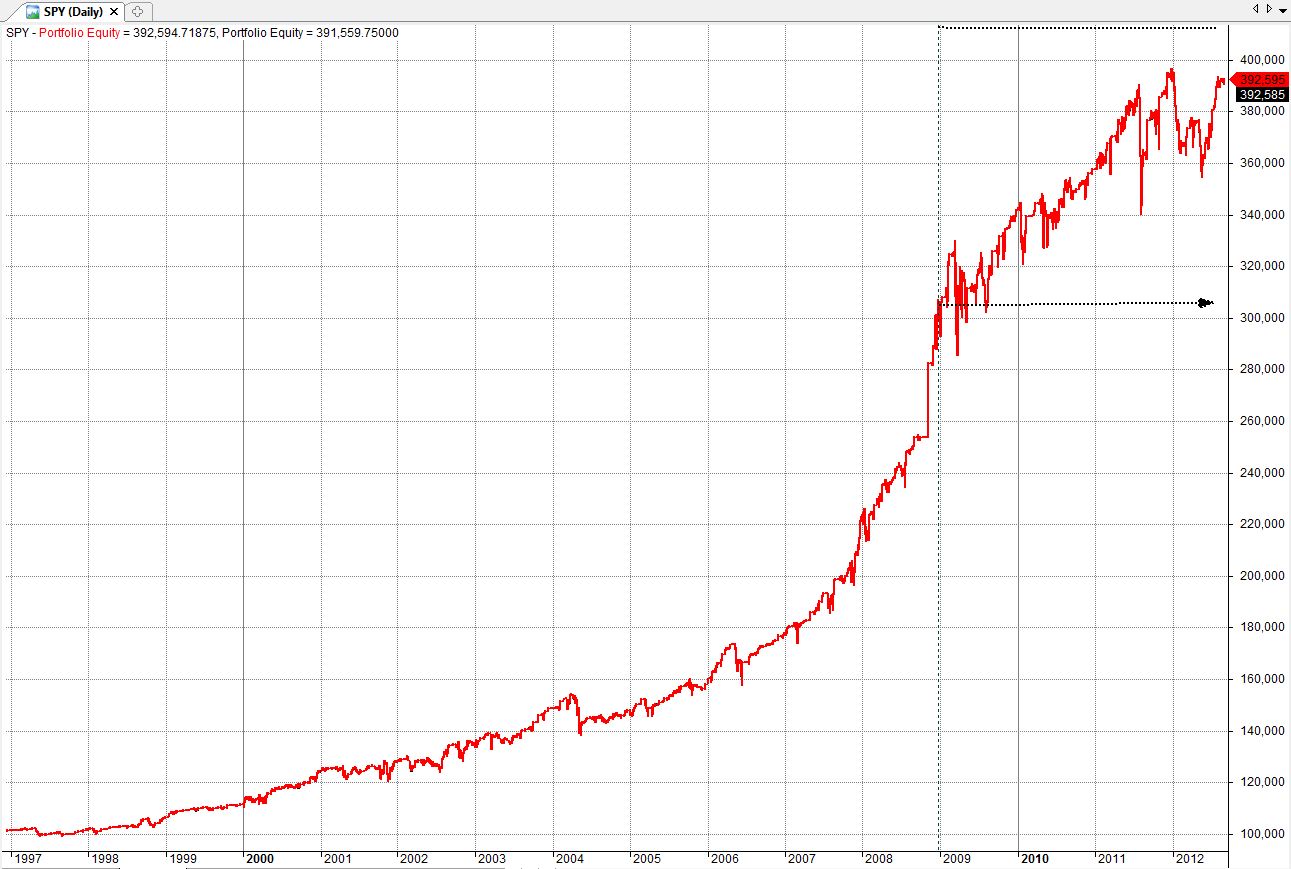

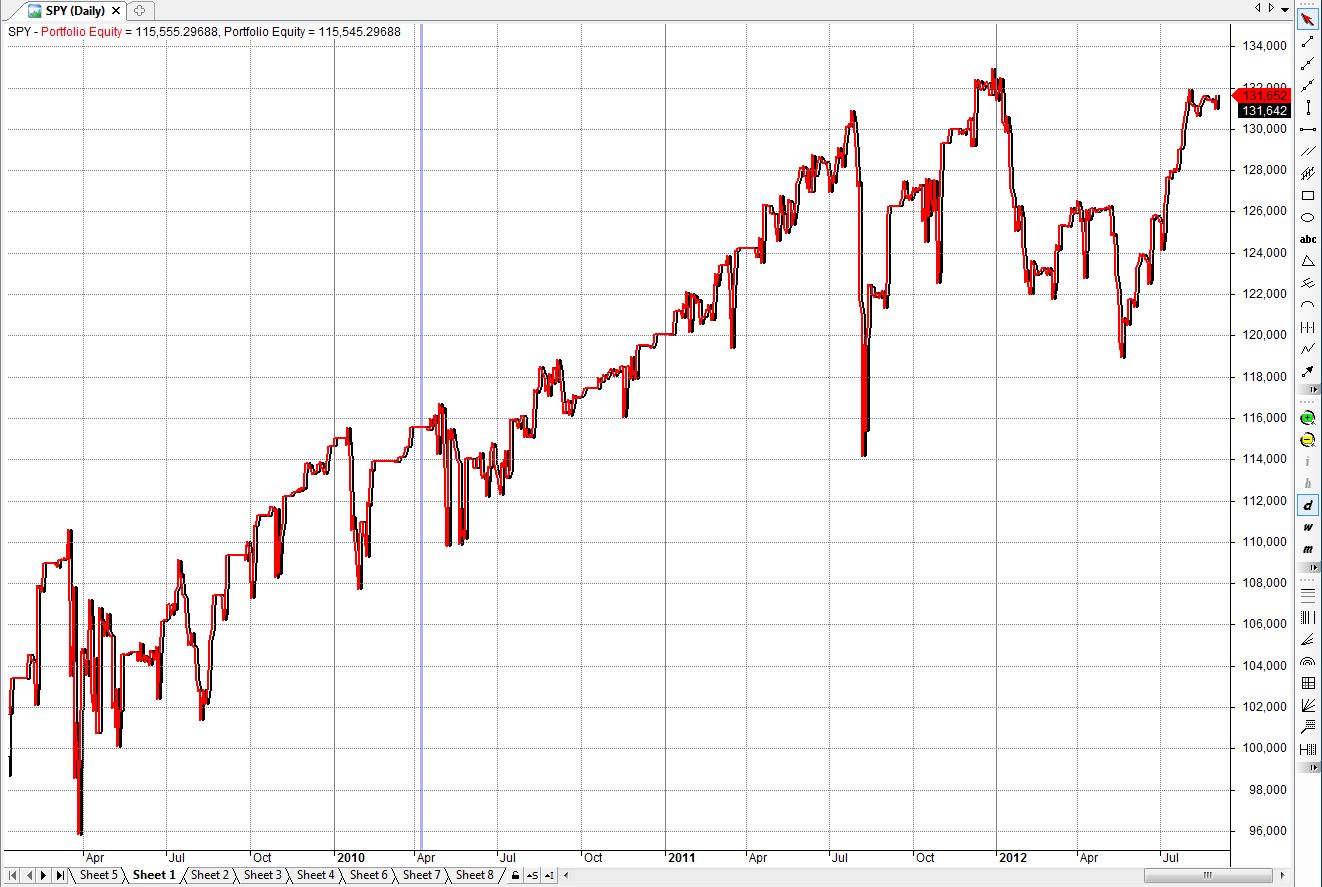

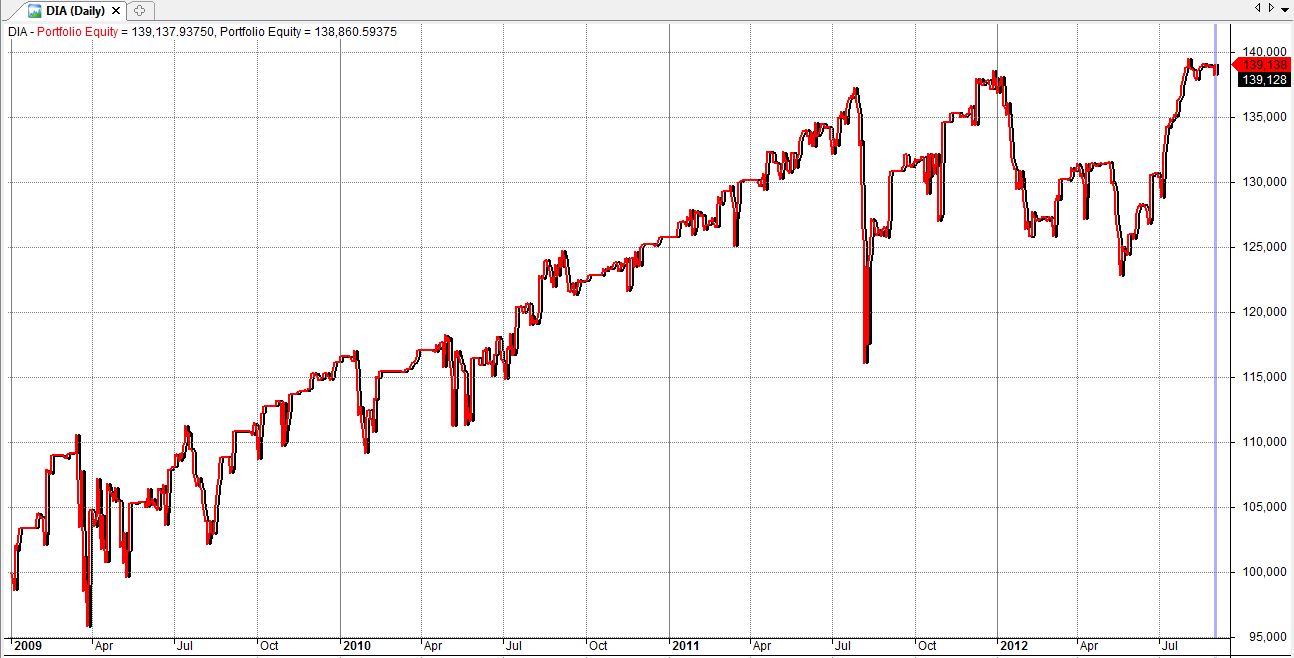

Read pt.1 REad pt.2 Back in 2009 Larry Connors and Cesar Alvarez published several short term trading systems in their book “High Probability ETF Trading". They described 7 mean reverting strategies. What happens, then once a strategy becomes public domain? Do they loose their edge? All tests are performed on a set of 20 ETFs:

DIA,EEM,EFA,EWH,EWJ,EWT,EWZ,FXI,GLD,ILF,IWM,IYR,QQQQ,SPY,XHB,XLB,XLE,XLF,XLI,XLV Tthe strategy can hold up to 10 ETFs at any time. Strategy 3: RSI 25-75 The rules: These rules are presented as found on the internet. Please refer to the original book for more info. ETF is above MA(200) 4 period RSI<25 BUY on the close of the day these criteria are met. *Aggresive version: Buy another unit if the 4-period RSI falls below 20 SELL on the close when 4 period RSI>55

For SHORT/COVER.

ETF is below MA(200) 4 period RSI>75 SHORT on the close of the day these criteria are met. COVER on the close when 4 period RSI<45

"Out of Sample" - 01/1/2009-9/5/2012 Profit = 31651.69 (31.65%), CAR = 7.78%, MaxSysDD = -16739.86 (-13.38%), CAR/MDD = 0.58, # winners = 376 (73.44%), # losers = 136 (26.56%)

*Aggresive Verion :"Out of Sample" - 01/1/2009-9/5/2012 Profit = 39137.94 (39.14%), CAR = 9.41%, MaxSysDD = -21294.28 (-15.50%), CAR/MDD = 0.61, # winners = 382 (74.61%), # losers = 130 (25.39%)

These results are good and trade-able at 8 to 9% annual return vs 13-15% draw-downs. Keep in mind these are "out-of-sample" results after the strategy has been published. Although they underperform the market (SP500) they have superior statistics (reward/risk) and will outperform when leveraged. * All tests performed are not guaranteed to be correct. Please verify any results for yourself. Amibroker code is available upon request.